SQM Research downgraded its national housing forecasts, citing stubborn inflation, rising energy costs, and the risk of further RBA rate hikes.

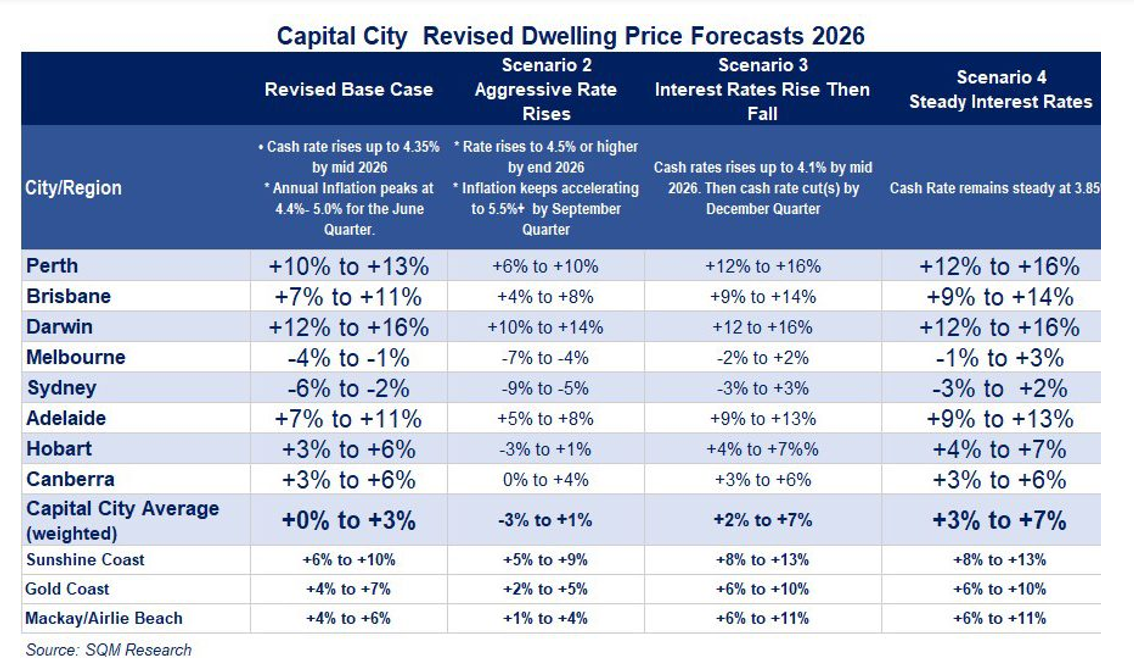

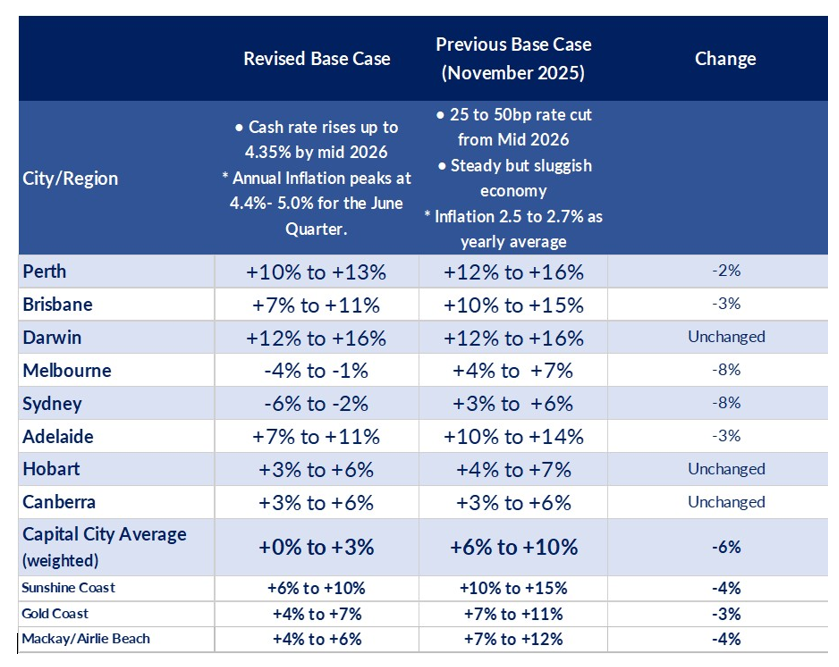

Weighted capital city dwelling prices are now tipped to grow by only 0 to 3%, compared with the previous 6% to 10% projection, tightening borrowing capacity for first-home buyers and property investors.

This comes after a year of strong price growth, with national home values rising 9% and February gains pushing the combined capital city median dwelling value above $1 million, according to the latest PropTrack data.

SQM notes that “weighted capital city prices are now expected to rise by just 0% to +3%, a significant downgrade from the November projection of +6% to +10%.”

The base case assumes the cash rate climbs to 4.35% by mid‑2026 and consumer price inflation peaks around 4.4 to 5% in the June quarter, keeping mortgage rates elevated for longer and limiting demand.

Against that backdrop, other forecasters such as KPMG still expect solid national gains of about 7.7% in 2026.

Escalating Middle East tensions and the risk of oil rising towards US$150 a barrel could further lift petrol and utility bills, eroding affordability and weakening buyer sentiment.

In this setting, Sydney prices are now forecast to fall 2 to 6% and Melbourne 1 to 4%, posing challenges for upgraders and leveraged investors.

By contrast, Perth and Darwin are projected to post double‑digit gains, supported by resources activity and population flows.

“While resource-heavy markets like Perth and Darwin hold firm, the downgrades in Sydney and Melbourne highlight vulnerability to higher rates,” said Louis Christopher (pictured), managing director of SQM Research.

Fresh figures from Cotality also suggest cheaper markets and mid‑sized capitals are leading the early‑2026 upswing, with buyer competition particularly focused on lower‑priced segments.

SQM’s alternative scenarios give brokers a clearer sense of the range of risks they may need to factor into client strategies. A more aggressive hiking cycle could drag national growth to between a 3% fall and a 1% rise, while a milder path or modest cuts would support stronger gains.

“Our revised forecasts reflect a more cautious outlook as energy-driven inflation risks mount, potentially delaying rate relief and weighing on housing demand,” Christopher said, adding that “Investors should monitor RBA signals closely amid these uncertainties.”

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.