ANZ and Macquarie Bank have moved in the opposite direction to most of the market, cutting fixed home loan rates at a time when the majority of lenders — including two of the big four — have been hiking.

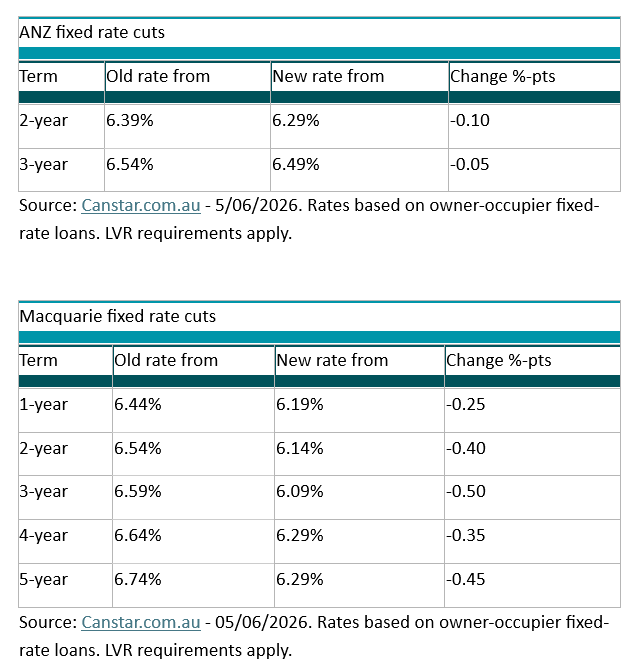

ANZ trimmed its two-year fixed rate by 0.10 percentage points to 6.29%, and its three-year rate by 0.05 points to 6.49%. Macquarie went further, slashing rates across all fixed terms by between 0.25 and 0.50 percentage points, landing its three-year fixed rate at 6.09% — the lowest of any of the five major lenders.

The rate cuts do little to close a widening gap between fixed and variable rates. At the start of 2026, 83 lenders on the Canstar database offered at least one fixed rate under 6%. That number has now fallen to just two. By contrast, more than 40 lenders still offer at least one variable rate below that threshold, and the lowest variable rate on the Canstar database currently sits at 5.69% through LCU.

The appetite for fixing has also dried up. According to the RBA's statement on monetary policy issued alongside its February 2026 rate decision, less than 5% of new and outstanding mortgages are currently on fixed-rate terms — down from a peak of almost 40% in early 2022 — underscoring just how far the fixed rate market has retreated since the pandemic era.

Canstar data insights director Sally Tindall said the two lenders had made a decisive move but cautioned that the broader fixed rate picture remained challenging.

"ANZ and Macquarie have today shifted gears, cutting fixed home loan rates at a time when the majority of the market is still trending up," Tindall said. "While these cuts are modest, they are enough to put Macquarie and ANZ in front of their big bank competitors."

She added that fixed rates remain a long way from competitive territory.

"Right now, there are just two lenders offering fixed rates under 6%. In contrast, there are over 40 lenders with at least one variable rate under this mark," Tindall said.

Canstar modelling illustrates the dilemma facing borrowers. On a $600,000 loan with 25 years remaining, a borrower taking the lowest 1-year fixed rate of 5.99% would be $1,798 worse off after 12 months compared to the lowest variable rate of 5.69%, if the cash rate remains on hold.

If the RBA delivers one further hike, the gap narrows — but variable still wins. Only if two more hikes materialise, as Westpac is forecasting, does fixing pull ahead — and only by $314.

"That slim margin highlights the challenge facing borrowers hoping to fix," Tindall said. "If rates stay on hold, the move is likely to cost them more. If rates rise further, fixing could potentially save money, but probably not enough to be considered a game changer."

The big four banks are sharply divided on where the cash rate goes from here. All four expect the RBA to hold at its meeting on 16 June. Beyond that, Westpac is forecasting two further hikes in August and September; NAB expects one more; while ANZ sees the cash rate as having peaked. CBA goes further still, pencilling in two cuts in May and August 2027.

For borrowers weighing a fixed rate, Tindall's advice is pragmatic.

"For many borrowers, the appeal of fixing isn't about securing the lowest rate, but instead, locking in certainty,” she said. “If that's you, spend time looking for a competitive offer before you lock in, and as always, read the fine print so you're fully across the limitations of a fixed rate mortgage."

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.