Australian private sector credit is still expanding at a solid clip, even as global financial stability risks rise and increase the chance of offshore shocks pushing funding costs and mortgage rates higher than currently assumed.

Westpac’s latest Australian Private Credit Bulletin shows total private credit rose 0.6% in February, up from 0.5% in January and in line with the average pace seen in 2025. Annual growth has climbed to 7.8%, a new high for this cycle. Housing credit, which makes up around 62% of total credit, also rose 0.6% over the month, a rate recorded in six of the past seven months.

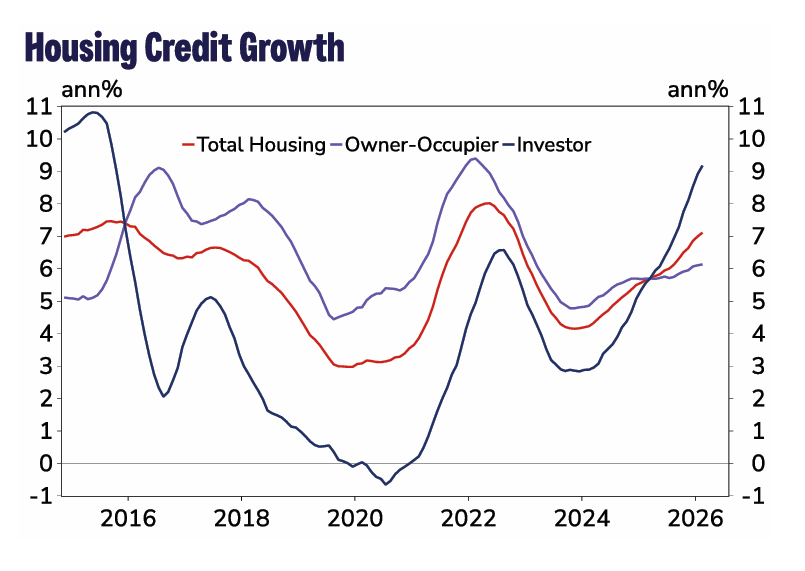

Senior economist Mantas Vanagas notes that “housing credit continues to be well supported” despite softer house price growth, weaker consumer sentiment, and changing expectations for interest rates. Ongoing supply shortages are helping to keep demand for finance robust even as conditions tighten.

The breakdown of housing credit shows familiar patterns.

Owner‑occupier credit recorded a thirteenth straight 0.5% monthly increase, indicating stable demand from first-home buyers and upgraders.

Investor credit growth eased slightly to 0.7% month‑on‑month, but Vanagas points out it was “very close to the rounding range for 0.8%mth,” underlining that property investors remain an important driver of new lending.

Elsewhere, other personal credit rose 0.4% in February, up from 0.2% in January, while business credit – about a third of total private credit – rebounded to 0.8%, matching last year’s average pace.

Looking ahead, Westpac warns that the backdrop is set to turn more challenging. The report flags the Middle East conflict and higher global energy prices as key headwinds, with a likely mix of high inflation, slower GDP growth, and softer labour market conditions.

“From March onwards, risks to credit growth are skewed to the downside,” Vanagas said.

Westpac now expects the Reserve Bank to lift the cash rate at the next three policy meetings – a path that would weigh on borrowing capacity, mortgage rates, and risk appetite for both first-home buyers and property investors.

Alongside this, APRA’s new debt‑to‑income limits on high‑multiple mortgages and closer scrutiny of commercial real estate and private credit are designed to keep lending standards prudent as household indebtedness remains high. This means brokers will need to navigate tighter guardrails even while credit is still available.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.