With just over a week until the next cash rate announcement, many economists still expect another increase. But Compare the Market economic director David Koch (pictured) argues the central bank should now pause, warning that sentiment among households and businesses has deteriorated sharply.

RBA is juggling multiple risks, including upcoming Consumer Price Index data, the 12 May federal budget, and the conflict in the Middle East, which is keeping oil prices elevated and feeding into inflation.

“They’ll be thinking about whether oil prices will stay high for longer, because if the Middle East crisis resolves itself, oil prices will drop significantly – and that would take a big chunk out of the inflation rate,” Koch said.

At the same time, he stressed the hit to confidence, pointing out that “consumer confidence has plunged and business confidence has fallen to almost record lows”. With the cash rate now at 4.1% after a 25-basis-point hike in March, weaker spending is already squeezing small businesses, while nervous employers are less likely to invest or hire.

For brokers, the implications are clear: first-home buyers and property investors are seeing their borrowing capacity eroded not only by earlier rate rises – with Canstar analysis indicating the latest RBA move has sliced about $12,000 off the average borrowing power – but also by soaring petrol costs. Koch argued that recent jumps in fuel prices have effectively worked like another cash rate hike.

“Because that interest rate increase – or the equivalent – has already come through in higher petrol prices, I reckon they might hold the line,” he said. “It’s a big call, but the week after is the federal budget, and they don’t know what’s coming there.”

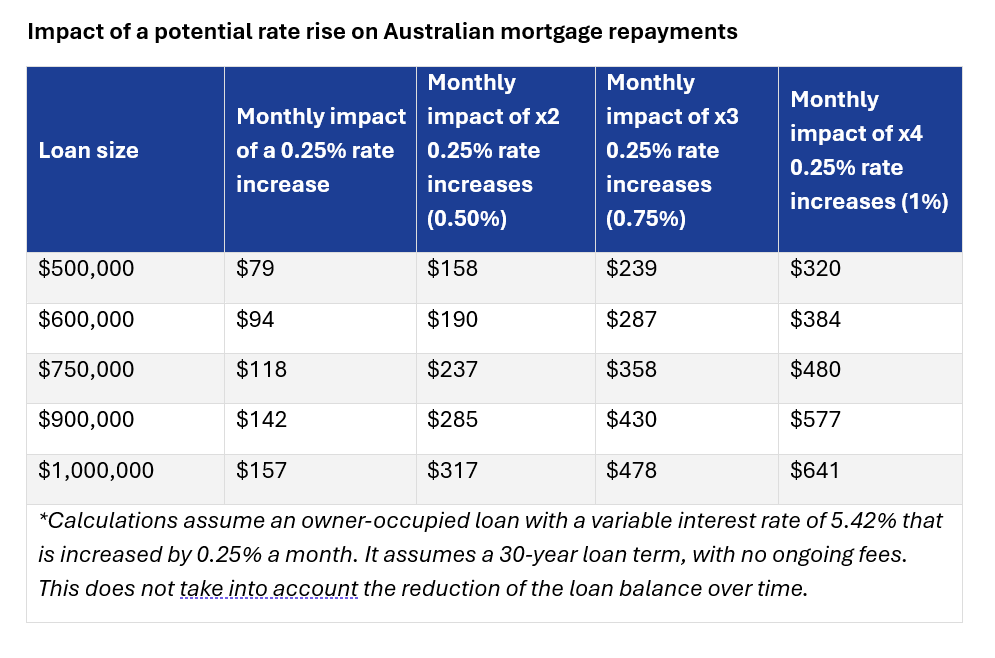

If RBA instead opts for another May increase, borrowers on variable mortgage rates could see repayments rise by hundreds of dollars a month, depending on loan size, adding further strain to already stretched budgets.

Koch urged Australians to “start plugging all of those financial leaks” in their household budgets, highlighting home loans as the first place to review.

“Number one: make sure you’ve got a home loan that suits your circumstances. If you don’t, do the numbers and consider refinancing,” Koch said, adding that households should also reassess major bills, from insurance to energy, to free up cash flow and soften the impact of any future mortgage rate moves.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.