Fixed mortgage rates have been edging higher while variable rate changes remain uneven, squeezing borrowing capacity for first-home buyers and property investors alike.

Canstar’s latest Weekly Rate Wrap-up points to a thinner pool of sharp deals and a more challenging environment for refinancing and new lending.

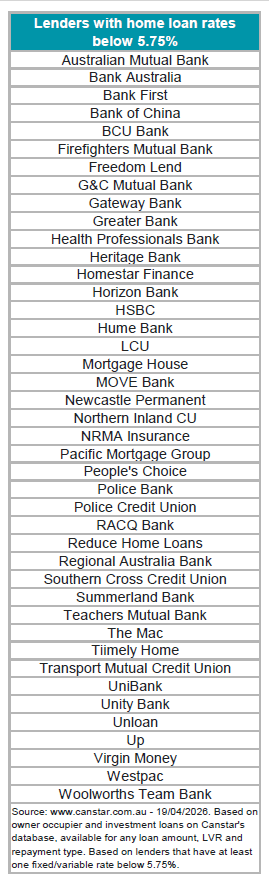

The pressure is most visible at the lower end of the market. There are now 89 home loan rates below 5.75% on Canstar’s database, down from 101 the week before, reducing the chances of substantially cutting repayments by switching. The average variable interest rate for owner-occupiers paying principal and interest sits at 6.42%, while the lowest variable rate for any LVR is 5.44%, offered by LCU.

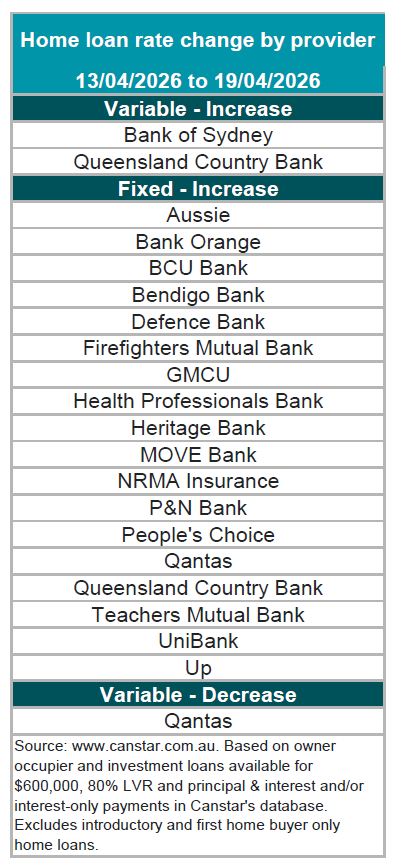

On fixed loans, lenders are still moving. Two lenders increased 18 owner-occupier and investor variable rates by an average of 0.25%, while Qantas Money cut four investor variable rates by 0.05%. More significantly, 18 lenders lifted 490 owner-occupier and investor fixed rates, with an average rise of 0.32%.

“The fixed rate hikes continue to roll in the door, albeit at a slower pace,” Canstar.com.au’s data insights director Sally Tindall (pictured) said.

Even so, one standout remains.

“Despite the rate rises, we’ve still got one fixed lender hanging tooth-and-nail on to a sub-5.5% rate,” Tindall said.

That is Northern Inland Credit Union’s one‑year fixed at 5.49%, with most lenders’ lowest fixed rates now above 6%.

Beyond headline mortgage rates, the broader backdrop is unsettled. Unemployment is steady at 4.3%, but expectations are for the jobless rate to drift higher later in the year.

At the same time, “Consumer confidence has fallen off a cliff since the start of the war and this is what the RBA will be most wary of, with the latest Westpac-Melbourne Institute data recording the biggest monthly decline since the onset of the COVID pandemic,” Tindall said.

With an already split RBA Board, brokers should prepare clients for shifting mortgage options and ensure strategies for both further rate rises and softer labour market conditions are front of mind.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.