Borrowers weighing up whether to fix or stay variable face a finely poised decision as inflation and geopolitical risks push rate expectations higher, according to new analysis from Canstar.

Canstar data insights director Sally Tindall (pictured) said the March quarter CPI, due this week, has Australia “in the brace position, with many economists predicting headline inflation will get precariously close to 5% in March, just one month into the war in the Middle East.”

Tindall warned the country “could well be back to a cash rate of 4.35%” if the Reserve Bank decides inflation pressures from the conflict require a stronger response.

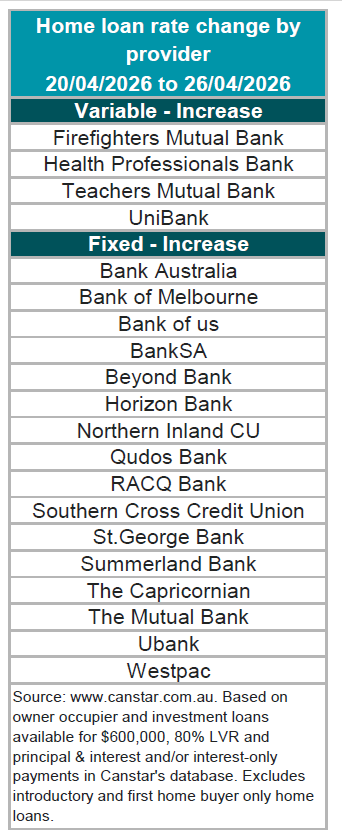

Fixed pricing is already moving ahead of the next RBA decision. Tindall noted that “fixed mortgage continued to climb last week”, with Northern Inland Credit Union withdrawing its 5.49% one‑year rate and the lowest one‑year fixed on Canstar’s database now 5.74% with Transport Mutual Credit Union.

To test whether borrowers have “missed the boat”, Canstar compared the average of the three lowest one‑year fixed rates (5.77%) with the average of the three lowest variable rates (5.51%) on a $600,000 owner‑occupier loan over 25 years.

If the cash rate does not rise again, the lowest variables come out ahead over the next 12 months, with about $1,558 less interest. Even with one 0.25‑percentage‑point hike, variable still wins, but only marginally, by around $187. Under a two‑hike scenario (May and June), fixing is ahead by roughly $1,058, and with three hikes (May, June and August) fixed borrowers are about $2,052 better off over the year.

At the same time, Canstar reports four lenders lifted 48 variable rates by an average 0.1% last week, while 16 lenders raised 315 fixed rates by an average 0.20%.

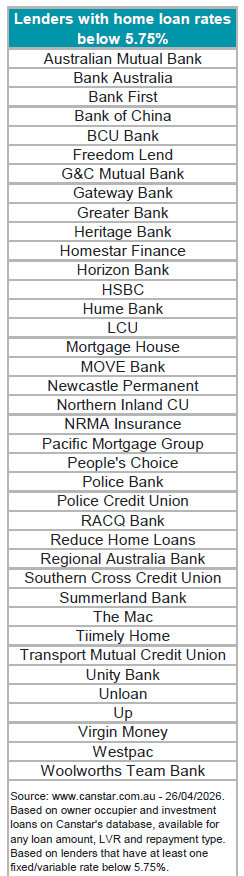

The average owner‑occupier principal‑and‑interest variable rate now sits at 6.42%, with the lowest variable at 5.44% and 82 rates below 5.75% on Canstar’s database.

Tindall cautioned that “making a decision to fix your mortgage rate when the stakes are quite finely balanced shouldn't solely be a bet on the cash rate; it should also take into consideration your personal financial situation and your personality to some extent.”

She urged anyone fixing to read the fine print, noting that many fixed loans do not offer offset accounts, cap extra repayments, and can carry “eye-watering break fees” if repaid early.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.