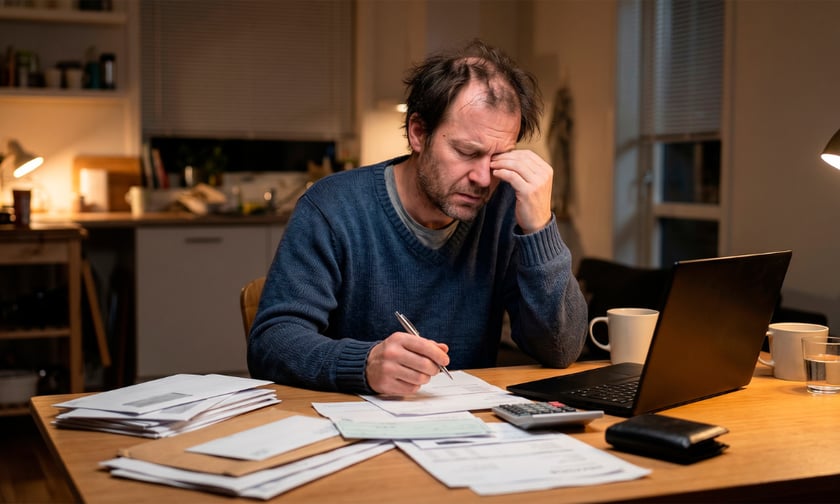

Household financial stress is no longer confined to the margins of the market.

New modelling from Digital Finance Analytics (DFA), cited by news.com.au and realestate.com.au, shows almost 2 million mortgage households and about 2.5 million renting households are in stress, where monthly outgoings exceed income.

DFA principal Martin North says that, assuming 10 million households, “just under half are in stress.”

In New South Wales, suburbs including Campbelltown, Riverstone, Gundaroo, and Mount Druitt all have 100% of mortgage‑holding households in stress, with Berwick and Essendon leading Victoria’s list. In Queensland, Pine Mountain, Highlands, Daisy Hill, and Tanah Merah are fully stressed, while Gawler East and South Plympton are the key hotspots in South Australia.

Fresh Roy Morgan data underscores how broad the challenge has become, finding 26.8% of mortgage holders – about 1,447,000 people – were “at risk” of mortgage stress in the three months to March, with 18.9% (around 1,020,000) classed as “extremely at risk”. Roy Morgan’s modelling suggests that share could climb to 30.9%, or roughly 1.66 million borrowers, by June if the Reserve Bank lifts the cash rate to 4.6%.

North warns that in some suburbs “most people are already in stress, which reduces economic activity, and home price growth.” If pressures persist, “expect more forced sales and home price falls,” he said.

Canstar’s Sally Tindall says another Reserve Bank hike would help get “the inflation job done, but at what cost” to borrowers, with consumer confidence already “sitting deep in the doldrums”.

Financial stress undermines clients’ decision‑making. ABC describes the effect as “poverty brain”, saying researchers found it was “the same as losing 13 IQ points”. When the financial stress leaves, “your decision‑making capacity bounces back”. For brokers, this means keeping advice simple and clearly documenting trade‑offs for anxious refinancers and first‑home buyers worried about mortgage rates.

Filipich urges people in distress to seek help from free financial counsellors via the National Debt Helpline, who cannot sell products and can negotiate hardship arrangements with creditors. For brokers, being able to refer vulnerable clients to this support is now a key part of responsible, long‑term client management.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.