Both banks’ economics teams updated their outlooks on Tuesday, pointing to stubborn inflation, stronger‑than‑expected economic growth and a blunt warning from the RBA governor that another rate rise is possible.

Their calls follow RBA’s December decision to hold the official cash rate (OCR) at 3.6%, while warning that “no cut was on the table” and that a hike in 2026 remains a real possibility if inflation fails to ease.

Canstar modelling shows even one RBA move would hit household budgets.

For an owner‑occupier paying principal and interest on a $600,000 loan with 25 years remaining, a single 0.25 percentage point hike would add $90 a month to minimum repayments. Two hikes – as NAB is forecasting – would lift monthly repayments by $180.

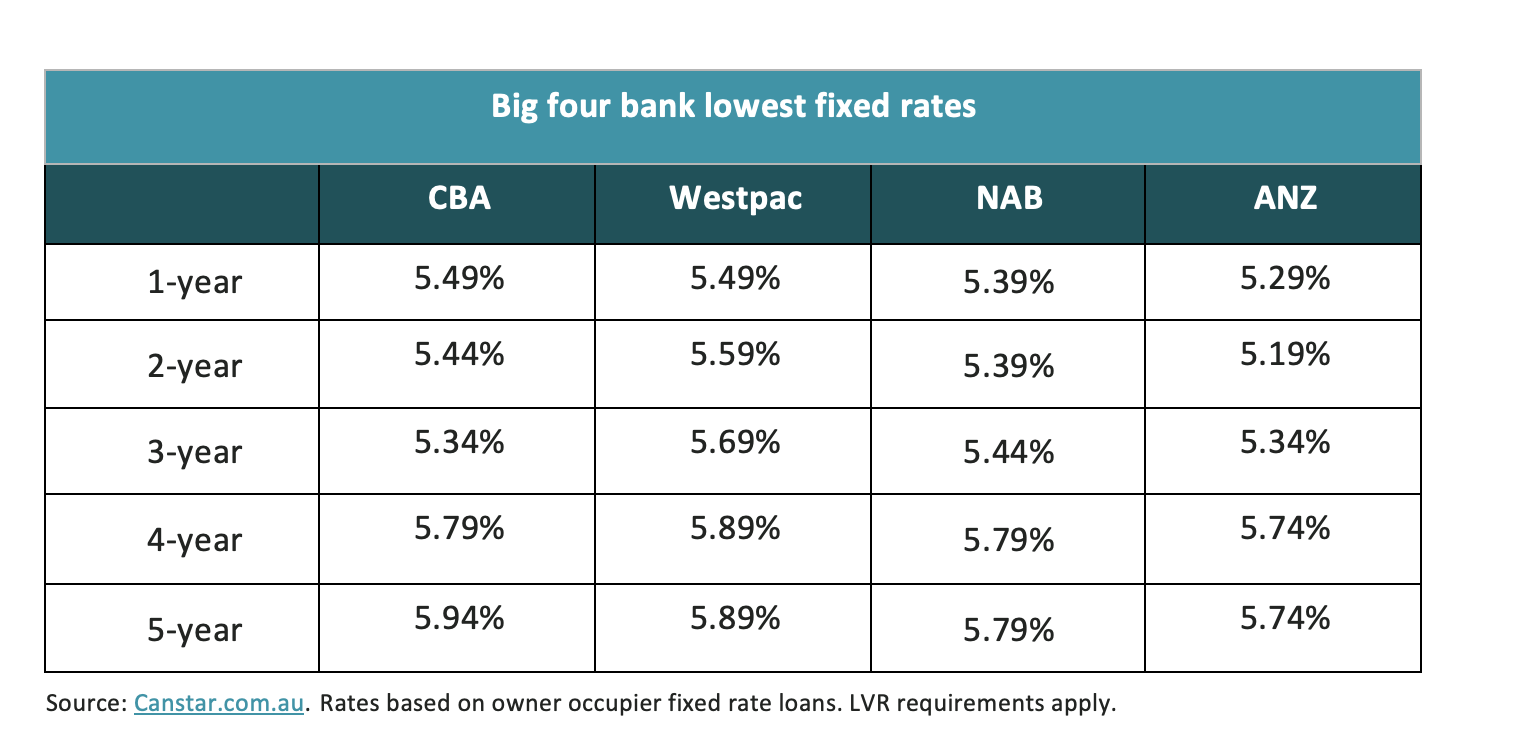

Fixed mortgage rates are already on the move. NAB has lifted fixed home loan rates by up to 0.20 percentage points, taking its lowest fixed rate to 5.39%.

The move follows Westpac’s fixed‑rate increases last Friday. As a result, ANZ now has the lowest fixed rates of the big four at 5.19% for two years.

The move follows Westpac’s fixed‑rate increases last Friday. As a result, ANZ now has the lowest fixed rates of the big four at 5.19% for two years.

Across the broader market, Canstar rate tracking shows 15 banks have upped at least one fixed rate since the RBA’s last meeting on 9 December.

Across the broader market, Canstar rate tracking shows 15 banks have upped at least one fixed rate since the RBA’s last meeting on 9 December.

Canstar data insights director Sally Tindall (pictured) said RBA’s recent messaging, combined with bank forecasts, should serve as a wake‑up call for borrowers.

“The RBA governor’s blunt warning last week put the nation formally on notice. Cash rate cuts are now behind us, and what’s in front could well be a rate hike,” Tindall said.

“Two of Australia’s biggest banks have joined the chorus, both suggesting the first hike could come as soon as February. By the time the RBA meets again in February, it will be armed with more data, including two additional monthly inflation prints and another employment report.

“However, if CPI doesn’t start tracking confidently in the right direction, the board could well be forced to act, particularly if the labour market continues to prove resilient under current interest rate settings.

“While these cash rate forecasts might not unfold exactly as planned, households with a mortgage should prepare for the possibility of hikes, and not just one.

“For someone with a $600,000 loan and 25 years remaining, two hikes next year could see their minimum monthly repayments rise by $180. Not exactly the 2026 borrowers were hoping for.”

Tindall said NAB’s change in cash‑rate outlook and fixed‑rate hikes underline how quickly pricing is shifting – and why borrowers should shop around.

“If you’re considering fixing, compare your options beyond the four walls of your big ban," the Canstar director said. "On a $600,000 mortgage, with 25 years remaining, the difference between opting for ANZ’s lowest two-year rate versus the lowest in the market translates into a whopping $4,773 in interest over the next 24 months. That’s not spare change – that’s a whole monthly repayment for many borrowers – just by shopping around.”

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.