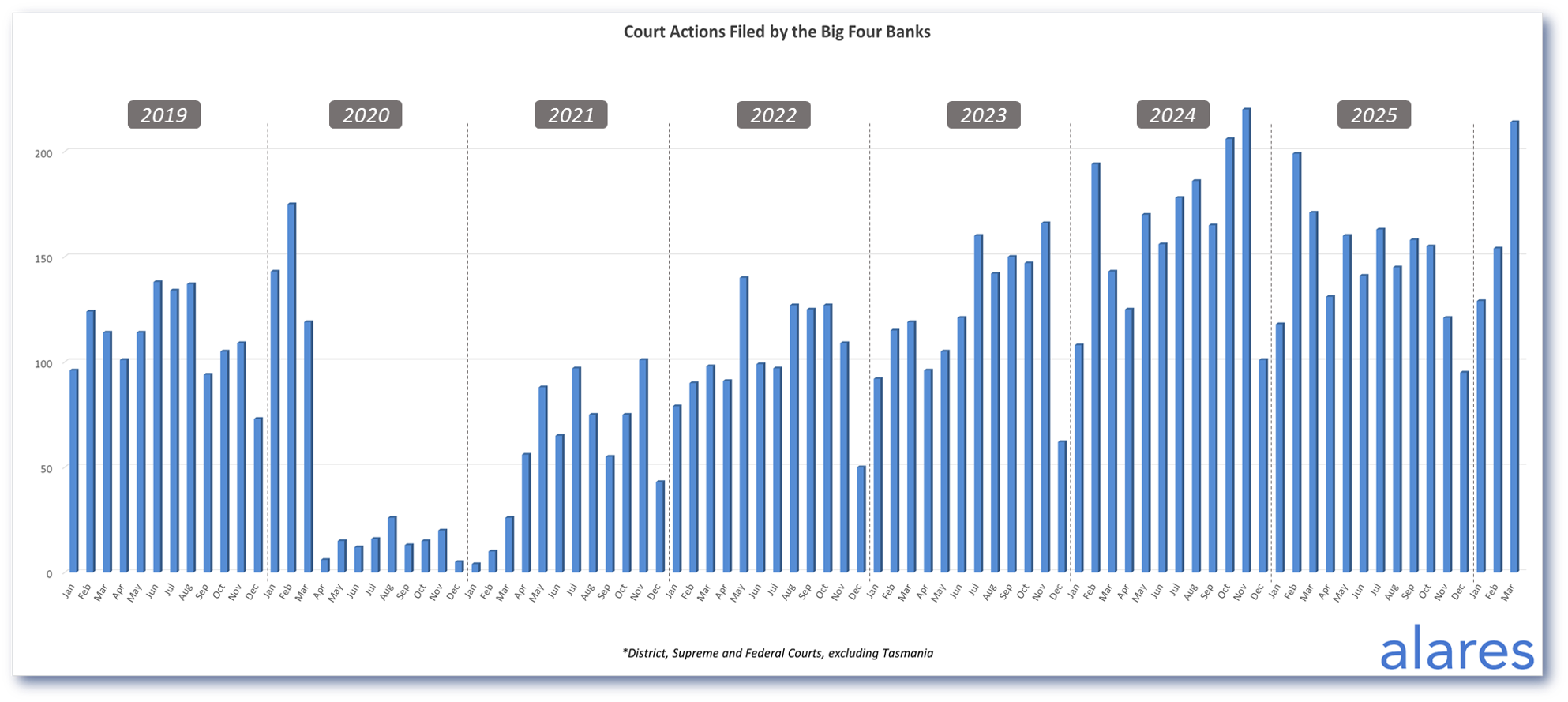

Australia’s Big Four banks are stepping up court‑led debt recoveries after a year of relative quiet, signalling a tougher credit environment for business borrowers and their advisers as business confidence remains fragile.

New analysis from Jirsch Sutherland, drawing on the latest Alares Credit Risk Insights, shows insolvencies holding near record highs in March alongside a sharp rebound in bank‑initiated court recoveries.

Partner Andrew Spring (pictured left) says the trend looks entrenched rather than temporary.

“The data suggests this isn’t a short-term spike, but a more sustained period of increased enforcement,” Spring said. “We’re seeing enforcement activity broaden significantly. It’s no longer concentrated in one area; the ATO, banks and other creditor providers are all active, creating a much tighter environment for businesses under pressure.”

Alares data highlighted in the report shows insolvencies remain elevated rather than “normalising” after the post‑COVID catch‑up, while Small Business Restructuring (SBR) appointments have plateaued. At the same time, ATO enforcement is staying active, including the use of public tax‑debt disclosure.

Alares director Patrick Schweizer (pictured right) notes that “March saw further increases in the ATO’s business tax debt disclosures, with more than 35,000 businesses now subject to ATO reporting”.

Spring says this visibility is reshaping how distress unfolds: “Greater visibility around tax debt means issues can surface more quickly, not just for the ATO but for other creditors as well.” That can shorten the window for borrowers to negotiate with lenders before multiple parties move to enforce.

While SBR volumes have eased, Jirsch Sutherland continues to see viable firms using the regime to stabilise and restructure. However, voluntary administrations are now roughly double pre‑2023 levels, signalling more businesses are reaching the point where formal intervention is unavoidable.

Spring warns that “with borrowing costs still elevated and margins under pressure, creditors are becoming less willing to wait and more likely to act”. The Reserve Bank of Australia’s March 2026 Financial Stability Review strikes a similar note, warning that many households and businesses are likely to see cash‑flow positions deteriorate over the next year as higher interest rates, elevated inflation, and a softer labour market bite, even though most are starting from relatively strong balance sheets.

Upcoming changes such as Payday Super could further compress cash flow, bringing forward distress for already stretched borrowers – and making early engagement with brokers and restructuring specialists more critical.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.