Australia’s business credit landscape is showing early signs of recovery, with fresh data from Equifax revealing credit scores at a three‑year high and larger enterprises leading the demand rebound.

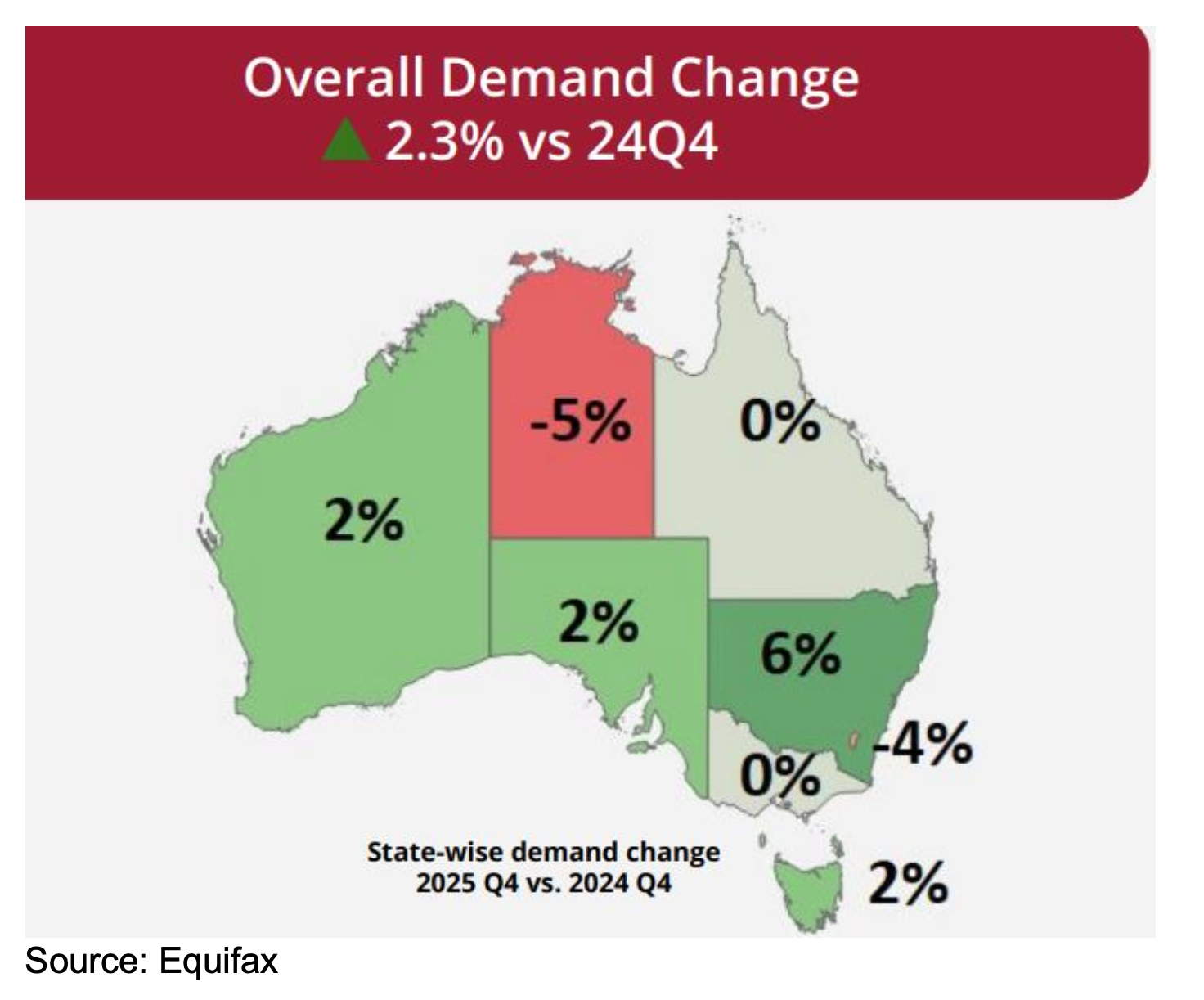

The Equifax Business Market Pulse for Q4 2025 shows overall business credit demand rose 2.3% compared to the same quarter in 2024, with business loan applications up 4.1%. Trade credit enquiries, however, fell 4.9%, suggesting fewer day‑to‑day transactions than a year earlier.

Brad Walters (pictured), general manager of commercial at Equifax, said the improvement in credit activity is being driven by a “multi‑speed” recovery.

“The +4.5% year-on-year increase in SME demand in Q4 2025 is a positive signal – though it reflects a more measured recovery pace compared to larger enterprises,” Walters said.

Equifax reports that business loan quality improved by two points in the December quarter, lifting overall business credit scores to their highest level in three years. Walters attributed this largely to who is seeking finance.

“When we look at the past quarter, it appears to be a story of a change in the market mix. We’ve seen more enquiries from larger businesses, which often have more reserves and carry higher credit scores,” he said. “This shift in the overall enquiry profile – where the larger players are currently more credit active than smaller players – is what I see driving this upward trend in credit quality.

“In practical terms, this shows that the credit quality of the mid-market and larger businesses overall remains quite resilient.”

Sector‑by‑sector, the gap between big business and SME appetite is most pronounced in hospitality, construction, and retail.

In hospitality, large operators significantly lifted demand across multiple products, including a 19.4% rise in trade credit enquiries, 9.1% growth in business loan demand, and a 5% increase in asset finance applications. SME demand in the same sector rose just 1.9% year‑on‑year, even as insolvencies declined 9% and average days beyond terms for trade payments improved slightly.

Construction showed a similar split. Insolvencies remained elevated and broadly unchanged, but Walters said the lending data “could suggest big builders are confidently securing materials for their project pipelines, driving a +6.6% year-on-year (vs Q4 2024) increase in trade credit.” By contrast, smaller construction firms trimmed overall credit demand by 0.7%, only lifting asset finance by 4% as they focused on borrowing for specific equipment.

In retail, national credit enquiries from large chains rose 7.9% year‑on‑year in Q4 2025, versus just 0.7% growth for SME retailers. Large New South Wales retailers were especially active, ramping up business loan enquiries by 25%. Yet underlying stresses remain.

“While we have seen strong demand growth among large retailers, the wider sector still shows some signs of pressure, with the past quarter revealing a substantial +64% increase in retail insolvencies year-on-year,” Walters said.

As borrowers digest these trends, the macro backdrop is turning more challenging. Recent Roy Morgan data shows business confidence slipping back below the neutral 100 mark, just as the RBA lifted the cash rate again in early February after hotter‑than‑expected inflation. With higher rates and weaker confidence, brokers say further RBA moves and softer sentiment could keep pressure on business borrowers and cash‑flows through 2026.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.