ANZ has revised its cash rate forecast, becoming the last of Australia’s four major banks to predict the Reserve Bank of Australia (RBA) will lift the cash rate to 4.10% in May – a move that could add hundreds of dollars to monthly mortgage repayments for Australian borrowers.

The bank’s economic team had previously expected the cash rate to remain on hold at 3.85%. The shift, announced on Thursday comes on the back of the latest Consumer Price Index (CPI) figures released the day prior.

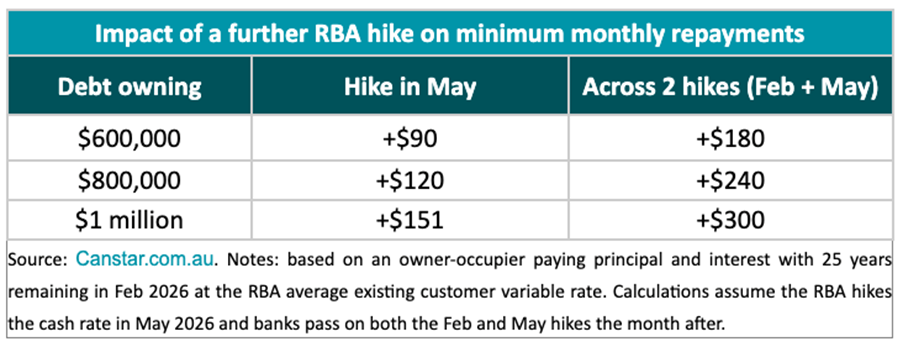

According to financial comparison site Canstar, a borrower with a $600,000 mortgage and 25 years remaining would see minimum monthly repayments rise by $90 if the May hike proceeds. Across two hikes this year – including the February increase – that figure climbs to $180 per month. For a $1 million loan, the combined impact across both hikes reaches $300 per month.

The development has also reignited debate over whether borrowers should lock in a fixed rate. Canstar’s analysis compared the average of the five lowest variable rates on its platform at 5.33% against the average of the five lowest two-year fixed rates at 5.31%. On a $600,000 loan over two years, fixing could save a borrower $239 even if rates remain unchanged. Should the RBA hike in May and hold thereafter, that saving could rise to about $2,842. Even if a cut follows in early 2027, fixed-rate borrowers could still come out ahead by $1,374.

Canstar.com.au data insights director Sally Tindall said ANZ’s change of position was prompted by the latest inflation data.

“ANZ was the last big bank holding firm on its view the RBA would only need a single hike to finish off the inflation job, but yesterday’s CPI figures have pushed the team to change their tune,” Tindall said.

“With all four major banks now pencilling in a May hike, borrowers should brace for the likelihood that rates aren’t quite done rising yet.

“Canstar analysis shows that even if there are no further cash rate hikes, one of the lowest two-year fixed rates currently on offer could end up cheaper than the lowest variable rate options over the next two years.

“If the RBA does hike again in May, the savings from fixing become more meaningful – potentially close to $3,000 in interest on a $600,000 loan, provided rates remain on hold thereafter for the rest of the fixed-rate term.

“With the equation largely on a knife’s edge and resting on a crystal ball at that, borrowers might be better off choosing what suits their finances, lifestyle and, in some cases, their personality.”

Official data show inflation has remained stubbornly above the Reserve Bank’s 2% to 3% target band, reinforcing expectations that policymakers may keep monetary settings tight.

Recent figures indicate annual consumer price growth remains elevated, driven by housing-related costs and ongoing price pressures across services. Underlying inflation – commonly measured by the trimmed mean and closely watched by the RBA – continues to sit above the midpoint of the target range.

Economists say sustained price growth strengthens the case for at least one additional rate increase this year, while also reducing the likelihood of near-term rate cuts. That outlook has contributed to banks revising their forecasts and adjusting mortgage pricing in response to changing expectations.

Major lenders have recently lifted fixed mortgage rates by up to 0.30 percentage points, reflecting expectations that borrowing costs could remain elevated for longer.

The moves by lenders such as Westpac and Commonwealth Bank signal growing caution in financial markets as inflation remains above the Reserve Bank’s target band. Analysts say banks typically price fixed rates based on expectations for future cash rate movements and wholesale funding costs rather than current policy settings.

The upward shift in fixed pricing has added to the broader debate about whether borrowers should lock in rates now or remain on variable terms, particularly as markets price in the possibility of further tightening in 2026.